Let's use this thread to discuss Apple Pay in Germany...

Experiences, developments etc. all in a single thread!

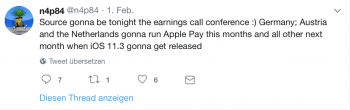

UPDATE: 31.07.2018 - Tim Cook confirmed that Apple Pay will launch later in 2018.

UPDATE: 05.11.2018 - Apple Pay DE site has gone live / showing "coming soon" + launch banks

UPDATE: 11.12.2018 - Apple Pay DE has gone live

--------------------------------------------------------

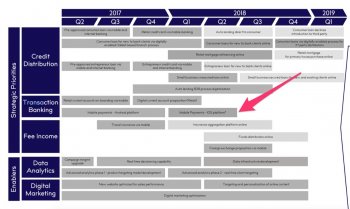

Supported banks at launch

Launching "soon" (2019)

Last updated: 11.12.2018

--------------------------------------------------------

Official Apple sites:

Experiences, developments etc. all in a single thread!

UPDATE: 31.07.2018 - Tim Cook confirmed that Apple Pay will launch later in 2018.

UPDATE: 05.11.2018 - Apple Pay DE site has gone live / showing "coming soon" + launch banks

UPDATE: 11.12.2018 - Apple Pay DE has gone live

--------------------------------------------------------

Supported banks at launch

- American Express

- boon. by Wirecard

- bunq

- comdirect

- Deutsche Bank

- Edenred

- Fidor Bank

- Hanseatic Bank

- HypoVereinsBank

- N26

- o2 Banking

- VIMpay (by Pay Center)

Launching "soon" (2019)

Last updated: 11.12.2018

--------------------------------------------------------

Official Apple sites:

- Apple Pay DE Official Site: https://www.apple.com/de/apple-pay/

- Apple Pay Supported Banks (Europe) overview: https://support.apple.com/en-gb/HT206637

- Apple Pay Supported Countries: https://support.apple.com/en-gb/HT207957

Last edited: